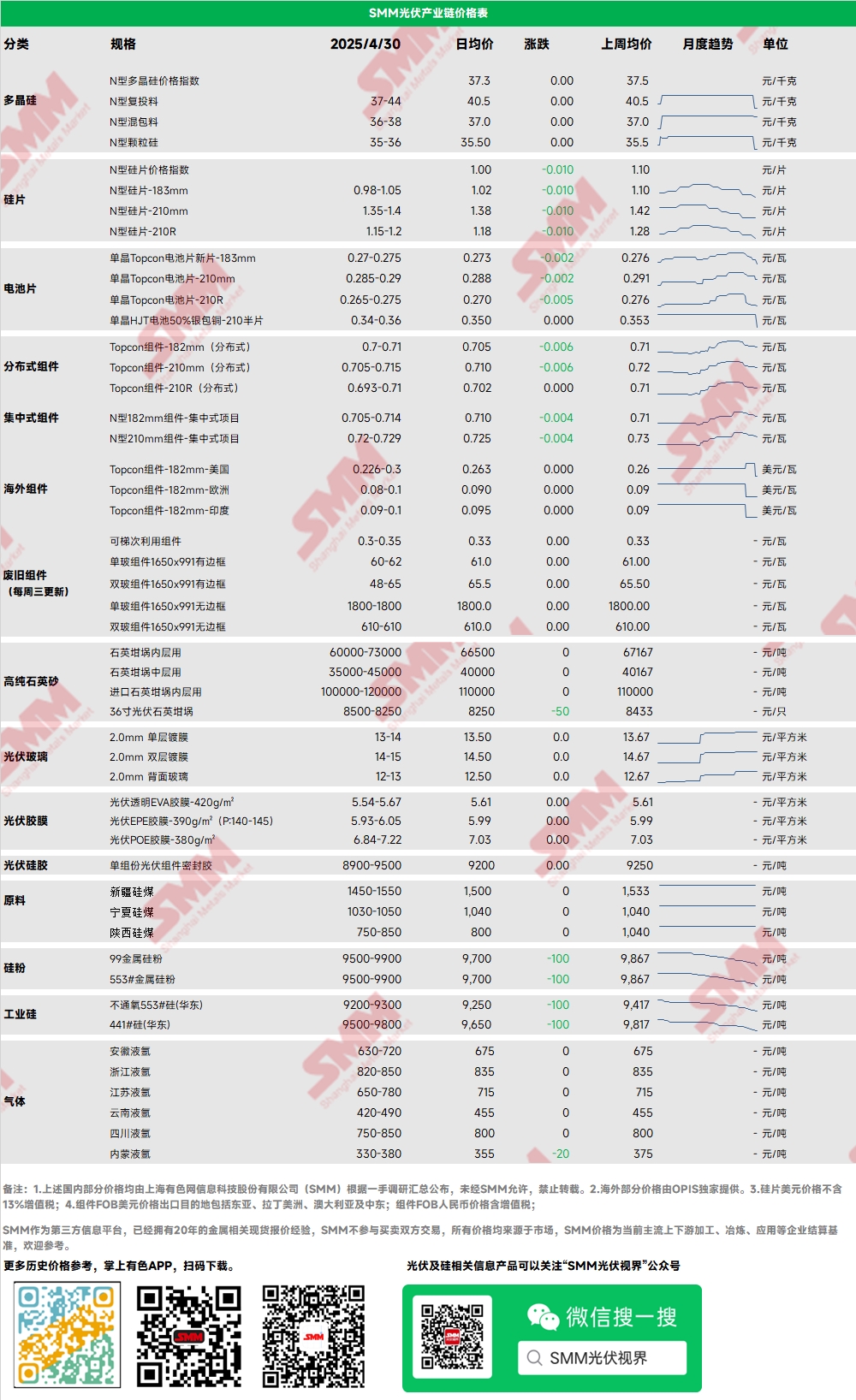

Polysilicon: This week, the mainstream transaction prices for N-type recharging polysilicon in the market were 37-44 yuan/kg, while those for N-type dense polysilicon were 36-40 yuan/kg. The N-type polysilicon price index was also noted. Polysilicon prices continued to decline this week, with the overall sentiment in the polysilicon market remaining weak. The center of transaction prices continued to move downward, with some top-tier polysilicon enterprises and traders seeing transaction prices fall by approximately 4 yuan/kg compared to quotes in early March. Some polysilicon enterprises may introduce new production capacity in May, but several enterprises are also expected to cut production. Overall, polysilicon production schedules in May are expected to decline MoM.

Wafer: This week, the prices for domestic N-type 183mm wafers were 0.98-1.05 yuan/piece, N-type 210R wafers were priced at 1.15-1.2 yuan/piece, and N-type 210mm wafers were priced at 1.35-1.4 yuan/piece. Wafer prices continued to decline this week. The overall market sentiment was poor, with downstream purchase demand remaining flat. Solar cell plants exhibited a clear "rush to buy amid continuous price rise and hold back amid price downturn" mentality. Wafer factory production schedules in May varied, with integrated enterprises increasing production due to operational inertia. Specialized enterprises, however, are expected to significantly cut production due to future concerns. Currently, it is anticipated that MoM production in May will decrease. Wafer supply is expected to remain below demand compared to battery production in May, which is expected to continue destocking. Combined with the relatively weak historical inventory pressure of wafers, this situation becomes a "hope" for wafers to stand firm on quotes. However, attention should also be paid to the subsequent price trends of polysilicon.

Solar Cell: This week, solar cell prices continued to decline, with the weekly average prices of Topcon 183, 210RN, and 210N falling by 4.53%, 2.5%, and 2.36%, respectively. The lowest quotation for 210RN this week was 0.265, approaching last year's low of 0.263. Panic selling sentiment emerged among solar cell enterprises, primarily due to the collapse of upstream prices and the lack of stabilization expectations, coupled with the continuous downturn in downstream module demand. The total production schedule in the market for May is close to 59GW, showing a MoM decline of about 9%. However, supply still exceeds demand on a monthly basis, and battery inventory is expected to accelerate growth.

PV Module: This week, PV module prices continued to decline. The mainstream transaction price for N-type 182mm modules in centralized projects ranged from 0.705-0.714 yuan/W, with the average price decreasing by 0.005 yuan/W. The mainstream transaction price for N-type 210mm modules ranged from 0.72-0.729 yuan/W, with the average price also decreasing by 0.005 yuan/W. The price of distributed N-type 182 modules was around 0.7-0.71 yuan/W, with the average price decreasing by 0.014 yuan/W compared to last Friday. The price of distributed N-type 210 modules ranged from 0.705-0.715 yuan/W, with the average price decreasing by 0.014 yuan/W compared to last Friday. The price of distributed N-type 210R modules ranged from 0.693-0.71 yuan/W, with the average price decreasing by 0.018 yuan/W compared to last Friday. This week, the price decline of distributed modules exceeded that of centralized modules, with some orders scheduled for May delivery already falling to 0.65-0.67 yuan/W (including freight). The actual transaction price of modules has approached previous lows, primarily because modules produced at this stage cannot be connected to grid before May 31. Enterprises are focusing on provincial PV policies, with the recent model of self-consumption and surplus electricity fed into the grid in Jiangsu Province bringing new opportunities to the PV industry. In summary, it is expected that PV module prices will continue to decline in May, but there may be strong support at the previous lows.

Terminal: From April 21, 2025, to April 27, 2025, SMM statistics showed that domestic enterprises won a total of 44 PV module projects. The winning bid prices for ordinary PV modules were concentrated in the range of 0.68-0.70 yuan/W, while those for perovskite PV modules were concentrated in the range of 1.80-1.89 yuan/W. The weighted average price of ordinary PV modules for the week was 0.69 yuan/W, a decrease of 0.03 yuan/W compared to the previous week. The total winning bid procurement capacity was 970.92MW, an increase of 228.42MW compared to the previous week.

EVA: This week, the price of PV-grade EVA ranged from 11,000-11,700 yuan/mt, with the average price falling by nearly 280 yuan/mt WoW. Prices for foaming-grade and cable-grade EVA also declined significantly, with transaction volumes slowing down and market sentiment remaining cautious. The installation rush in the demand side is coming to an end, with demand clearly slowing down. Additionally, there are expectations of a decline in new order prices for film in May. The narrowing price spread between film and particles is forcing the raw material side to make concessions. With demand gradually weakening, it is expected that EVA prices will continue to decline under pressure.

Film: The mainstream price range for EVA film is 13,300-13,500 yuan/mt, while the price range for EPE film is 15,200-15,500 yuan/mt, with prices remaining stable. With the continuous decline in module prices and gradually weakening demand, the downward trend in the price of PV-grade EVA on the cost side provides cost support for new film orders in May. The pricing of new film orders in May is still under negotiation, with expectations of a decline.

POE: The domestic delivery-to-factory price of POE remains stable at 12,000-14,000 yuan/mt. Despite maintenance at some petrochemical plants, the dual impact of the approaching end of the installation rush in the PV industry and the release of new production capacity is expected to put downward pressure on the price of PV-grade POE.

PV Glass: This week, some PV glass enterprises have reduced their quotations. Currently, the mainstream quotation for 2.0mm single-layer coated PV glass in China is 13.5 yuan/m², with few transactions. The mainstream quotation for 3.2mm single-layer coated PV glass is 22.0 yuan/m², and the mainstream quotation for 2.0mm back-side PV glass is 12.5 yuan/m². This week, some PV glass enterprises began to reduce their quotations. As the negotiation period for new orders in May approaches, glass enterprises, influenced by the expected weakening of subsequent demand, have started to make slight concessions to destock this week. Against the backdrop of extremely poor acceptance sentiment among module enterprises at high prices and a strong desire to bargain down prices, it is expected that the price of new order glass in May will be slightly reduced.

High-Purity Quartz Sand: This week, the high prices of some domestic high-purity quartz sand products have slightly declined. Current market quotations are as follows: inner-layer sand is priced at 65,000-73,000 yuan/mt, middle-layer sand at 35,000-45,000 yuan/mt, and outer-layer sand at 18,000-25,000 yuan/mt. This week, domestic wafer prices have begun to decline significantly, and wafer production schedules are limited. Meanwhile, the impact of trade war tariffs has recently begun to weaken, leading to a decline in the high prices of imported sand in the market and a weakening of sentiment support. The substitution tension of domestic quartz sand has slightly eased. Against the backdrop of declining wafer prices, the purchase willingness of crucible enterprises for quartz sand has also decreased, with strong resistance to high prices. Therefore, market quotations have slightly declined this week. It is expected that the subsequent center of transaction prices will still decline appropriately due to the weakness of both wafer prices and production schedules.

》View the SMM PV Industry Chain Database

![[SMM PV News] Armenia Hits 1.1 GW Solar Capacity,](https://imgqn.smm.cn/usercenter/qQwIB20251217171741.jpg)

![Spot Market and Domestic Inventory Brief Review (February 5, 2026) [SMM Silver Market Weekly Review]](https://imgqn.smm.cn/usercenter/tSwaX20251217171735.jpg)